If you're seeing higher earnings, ask yourself: has risk increased? If so, why?

Supply and demand in real markets affect returns by normalizing prices. When a trading session produces more earnings, the pair is usually more volatile: one asset is moving toward a higher risk tier and the other toward a lower one.

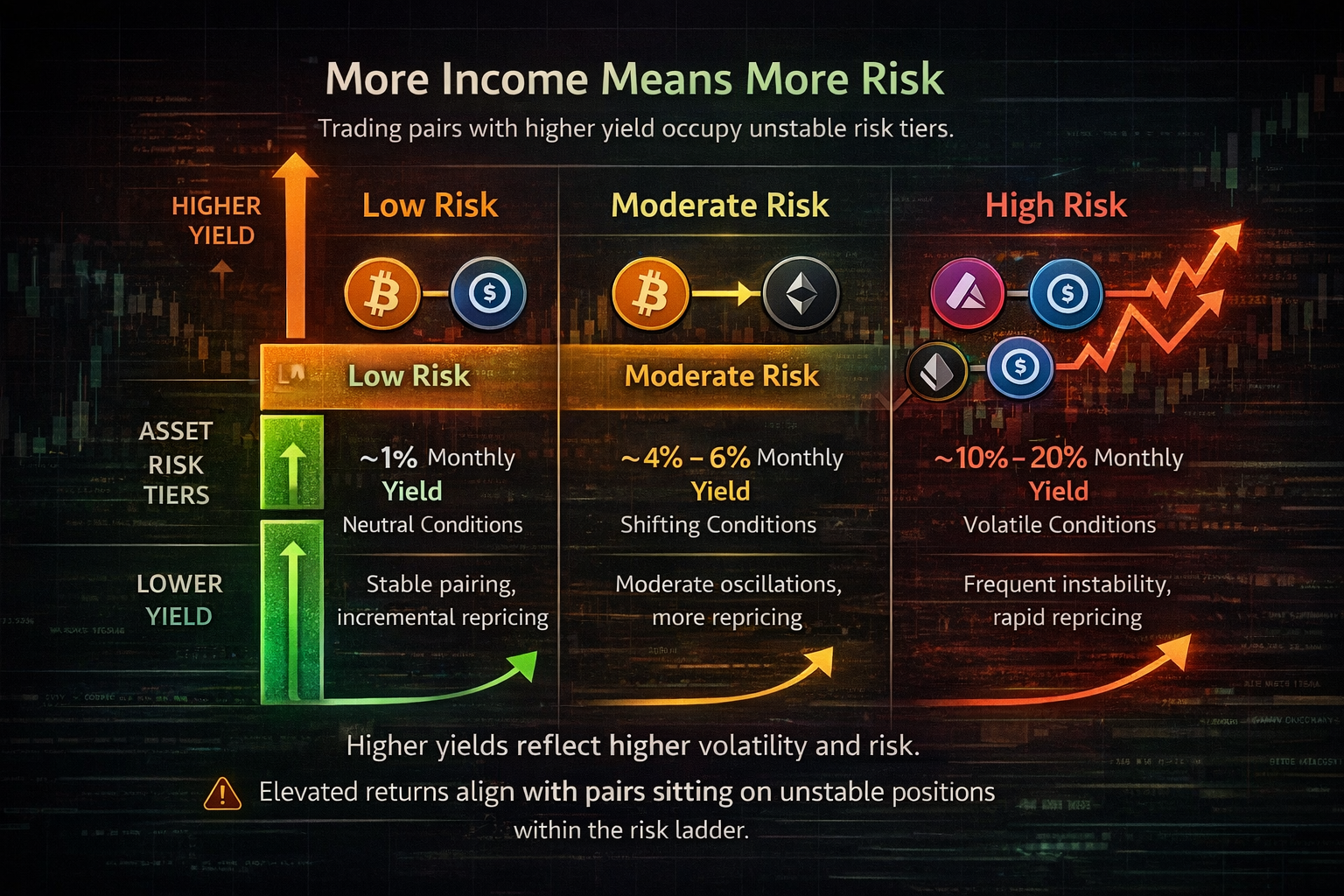

That's why BTC/USDC might yield around 1% monthly, major coins 4–6%, and higher-risk coins 10–20%. The lower-yield assets are less volatile—their relative risk changes less often. The higher-yield ones earn more precisely because they are more volatile and their risk profile shifts more frequently.

These percentage returns are directly linked to the ladder position of the two underlying assets, averaged out for the pair. If you trade the highest position with the second highest (e.g. BTC/ETH), your risk profile should in theory be the lowest possible among pairs.

These are rough estimates. Actual returns depend on market conditions, grid settings, and capital deployed. The point: higher earnings are not free—they reflect higher volatility and risk.

If you are seeing higher earnings, the first question is not "how can I scale this?" It is: what changed in the risk profile? Returns do not increase in isolation. They are a function of volatility, capital rotation, and relative repricing between assets.

In real markets, supply and demand continuously normalize inefficiencies. If a pair suddenly produces higher returns, it is not because the market became generous. It is because price displacement increased. One asset is climbing the risk ladder, the other is descending. That relative divergence is what creates opportunity.

A trading session with elevated earnings usually coincides with elevated volatility. Volatility is not random noise. It represents repricing of perceived risk. When an asset migrates to a higher risk tier, it does so because uncertainty increased: liquidity thins, spreads widen, reaction speed accelerates. The opposite occurs for the counter-asset.

This is why pairs like BTC/USDC often yield around 1% monthly under neutral conditions. Bitcoin against USD Coin is structurally constrained. One side is relatively stable by design. The relative risk differential does not shift aggressively or frequently. Lower volatility, lower structural yield.

Move to major coins and the dynamic changes. Ethereum paired with BTC may yield 4–6% because both legs fluctuate, but within relatively mature liquidity conditions. Risk tiers shift, but not violently.

Now move further down the ladder into higher-beta altcoins. Here you see 10–20% potential. Not because they are superior. Because they are unstable. Their volatility regime changes often. Their ladder position reorders frequently. That instability is the income source.

These percentage ranges are not arbitrary. They are a function of the average ladder distance between the two underlying assets over time. Every asset occupies a dynamic position in a relative risk hierarchy. When you trade a pair, you are effectively trading the spread between two ladder positions.

The wider and more unstable the spread, the higher the potential yield. But that spread instability is precisely the risk. Frequent re-ranking means frequent regime shifts. If you do not understand where each asset sits and how fast it migrates, your backtest results become misleading.

If you trade two assets at the top of the ladder, such as BTC/ETH, the theoretical relative risk is lower than BTC versus a small-cap token. Their volatility profiles are more correlated. Their capital bases are deeper. Their repricing is more incremental. That reduces structural divergence and therefore reduces yield potential.

Higher income is compensation for absorbing faster and more frequent changes in relative positioning. It is not free return. It is payment for tolerating instability.

When you see a high percentage in a backtest, isolate the source:

- Is it concentrated in short volatility bursts?

- Is it distributed across regimes?

- Does it depend on extreme ladder shifts?

If most profits come from short periods of abnormal volatility, then your risk is regime-dependent. If earnings are smoother and more evenly distributed, the risk profile is more stable.

In practical terms: income is a derivative of volatility, and volatility is a derivative of perceived risk. The market does not pay more without demanding something in return. If your yield increases, your exposure has changed. Identify how and why before increasing size.